Financial Goals for Men in Your 20s and 30s: A Planning Framework

Here is a number that should bother you. According to Fidelity's retirement readiness benchmark, most men should have roughly one times their annual salary saved by age 30 and three times by age 40 to be on track for a comfortable retirement. The actual median for American men in those age brackets is a fraction of that. The gap isn't a discount rate problem or a markets problem. It's a planning problem. Men in their twenties and thirties know in the abstract that money matters. They just have no structure for turning that knowledge into monthly action. This is the framework that fixes that.

Why Financial Goals Feel Abstract (And Therefore Get Ignored)

Ask most men what their financial goals are and you will get something like "I want to save more" or "I want to buy a house." Both are gestures, not goals. Neither tells you what to do on Tuesday morning. Your brain cannot act on a gesture. It can only act on a specific amount, a specific account, a specific date, and a specific source of funds.

A real financial goal has four components. The number. The deadline. The account. The funding rule. "Save more" has none of them. "Deposit €400 from salary into the Revolut Savings pot on the 1st of every month until the balance reaches €12,000" has all of them. The second one you can execute. The first one you cannot.

This is also why financial goals almost never stick when they live only in your head. They have to live somewhere physical where your weekly review forces you to see them. Men who track financial goals in a planner or a spreadsheet hit their targets at roughly twice the rate of men who hold them mentally. The writing is the commitment. The reviewing is the maintenance.

The Three-Horizon Framework for Financial Goals

Money operates on different time horizons, and the reason most financial goal systems fail is that they mash those horizons together. The fix is to separate them cleanly and plan each one on its own schedule.

The first horizon is today and this month. This is your cash flow layer. The non-negotiables are simple: you know what came in, you know what went out, and you know what stayed. If you cannot answer those three questions for the last thirty days inside two minutes, you do not have a cash flow system. You have a cash flow hope. The monthly check takes fifteen minutes and it is the price of admission to all the other horizons.

The second horizon is tactical, the twelve-to-thirty-six-month window. This is where emergency funds live, big purchases live, debt payoff lives, and the first real pots of investable cash come together. Most men skip the cash flow layer and try to plan here directly, and then wonder why the plan never survives an unplanned expense. You cannot plan the tactical layer if the cash flow layer is leaking.

The third horizon is strategic, five to thirty years. This is retirement, property, long-term investing, the trajectory of your career. The strategic layer does not need weekly attention. It needs quarterly attention. What it does need is to be consistent with the tactical layer, which in turn needs to be consistent with the cash flow layer. When the three horizons are aligned, money problems get solved in the right layer. When they are not, men spend years patching leaks that only exist because the underlying structure is wrong.

Financial Goals for Men: The Four Non-Negotiables

Before you set specific goals, four structural positions need to be true. Everything else is optimisation.

One. You have an emergency fund equal to at least three months of your current monthly expenses, in a separate account you cannot accidentally spend. This is the floor. Every man who has ever skipped the emergency fund has paid for it inside three years. Without it, every other financial goal you set is fragile, because one bad month wipes the year's progress.

Two. You have no revolving credit card debt. Any balance you are carrying month to month at standard credit card APRs is a tax you pay for not having a plan. This gets handled before any investment goal is set, because there is no investment return in the world that reliably outpaces a 22 percent interest rate. Structured debt like a mortgage or a cheap personal loan is a different conversation. Consumer credit card debt gets killed first.

Three. You are contributing to any retirement match your employer offers. Free money is free money. If your employer matches up to six percent, you contribute at least six percent from the day you understand that sentence. Not doing this is the single most expensive financial mistake a man in his twenties or thirties can make, because it compounds for thirty years.

Four. You have a simple low-cost investing account set up and funded by automatic transfer. The account is more important than the strategy. Men who have an open account and no plan outperform men who have a brilliant plan and no open account, because the men with no account never get around to opening one. Open it today. Fund it with something trivial like €50. The structural position matters.

How to Set Financial Goals That Actually Get Hit

Once the four non-negotiables are in place, goal setting gets simple. Pick one financial goal per horizon per quarter. One cash flow goal. One tactical goal. One strategic goal. Not twelve. Three.

The cash flow goal is usually a habit goal. "Complete the monthly money review on the first Sunday of every month, for the whole quarter." That is a goal you can objectively pass or fail. The review itself looks at categories, identifies one place where leakage is happening, and sets a specific reduction for the next month.

The tactical goal is usually a number with a deadline. "Build emergency fund from €2,000 to €8,000 by September 30." To get there, you back-calculate what needs to move from each paycheque into the emergency account. That amount becomes an automatic transfer the day after you get paid. Automation is what makes the goal reliable. Willpower is what makes it fail.

The strategic goal is usually a positioning goal, something like "Increase retirement contribution from six percent to eight percent of salary starting in the next pay cycle, and hold it for the rest of the year." You are not chasing market returns. You are moving the strategic layer one notch better and letting time do the rest.

Three goals. One per horizon. Reviewed monthly in your planner. That is the entire system.

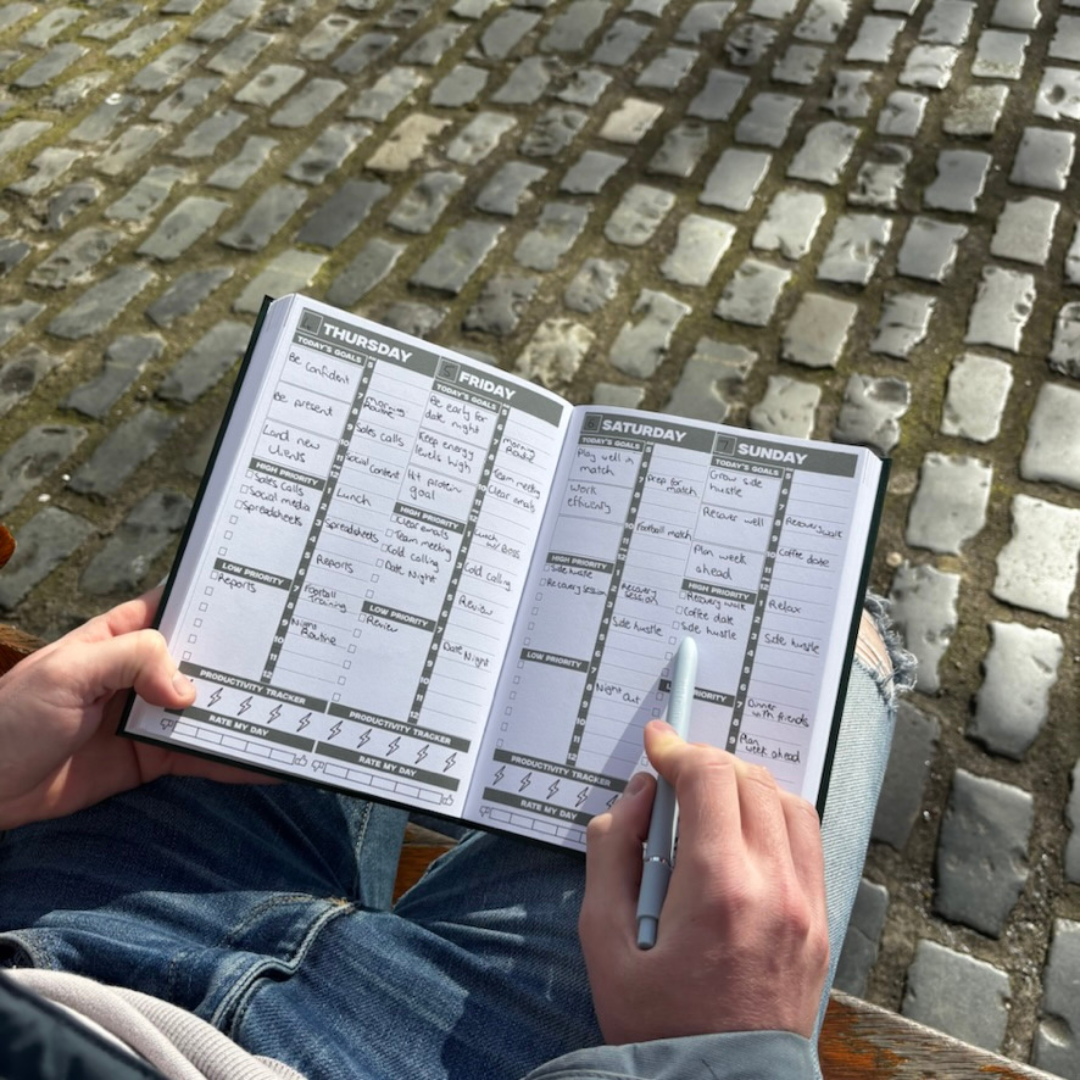

Putting Financial Goals in Your Planner (And Why Paper Wins)

Every financial app on earth will show you a dashboard. Almost none of them will make you sit with your money the way a pen on paper does. There is something about writing "balance on October 1: €4,312" in ink in your planner that makes the number real in a way the app never does. Apps you glance at. Planners you engage with.

The Plan Your Growth undated weekly agenda has the structure for exactly this. Space on the weekly spread to write your three quarterly goals at the top so you see them every Monday. Habit tracker at the bottom for the automatic check-ins (did you do the monthly review, did the transfer run, did you log the numbers). Undated so you can start this system tomorrow instead of waiting for January.

The review itself is simple. Once a month, thirty minutes with a cup of coffee. Open the agenda. Open your banking app. Write the closing balances in each of your tracked accounts. Compare to the prior month. Note one thing that went well. Note one thing you want to change next month. Close the agenda. That is the entire process. It compounds more wealth than most financial products will.

How to Stay Consistent When Life Gets Expensive

The test of a financial plan is not the month you made it. It is the month a wedding, a medical bill, a car repair, and a birthday all land in the same four weeks. That is where most men quietly abandon the plan and go back to financial drift. Here is what actually holds.

First, protect the automatic transfers no matter what. The biggest risk in an expensive month is that you pause the standing transfer to the emergency fund or the investment account "just this once." Do not. The automation is what is doing most of the work, and turning it off is how you undo a quarter of progress in a single click. Expensive months come out of the joy bucket, out of delay on non-urgent purchases, out of negotiating payment plans. They do not come out of the structural layer.

Second, have a pre-decided answer for the unexpected €500 expense. Most men decide what to do in the moment, and in the moment, the emergency fund is the obvious source. If you are using the emergency fund every two or three months for things that are not emergencies, it is not an emergency fund, it is a spending account with a different name. Decide in advance: true emergency (job loss, health, urgent home repair) comes from the emergency fund. Everything else comes from the joy bucket or gets delayed.

Third, do not let a bad month become the reason to skip the monthly review. The review is especially valuable after a hard month because that is when you see the mechanism. What exactly blew the plan? Was it one outlier or a pattern? Was it truly unexpected or foreseeable? The review turns a bad month into useful information. Skipping the review is how a bad month becomes a bad quarter.

The Bottom Line

Financial goals fail for men in their twenties and thirties because the goals are vague, the horizons are confused, and the system lives in their head instead of on paper. Fix all three and your finances get structural. Use the three-horizon framework to separate cash flow from tactical from strategic decisions. Lock in the four non-negotiable structural positions before you optimise anything. Pick one goal per horizon per quarter, automate the funding, and review monthly. Write the balances in ink. Do that for three years and the net worth chart stops looking like a flat line.

If you want the structure on paper so the monthly review is the easiest thirty minutes of your month, the Plan Your Growth undated weekly agenda is the operating system for it. Weekly goal spread, habit tracker, undated pages so your first monthly review can happen next Sunday instead of next January. Pick a colour, pick an account to track, and give this quarter a real target.